Article 4 of 5 | Following our May 2026 Chartwell webinar

Most utilities know when a customer is already in arrears. The harder question is whether they can see which customers are heading there before the debt becomes significant enough to say so.

That gap is where the model needs to change.

The limitation that traditional collection models cannot solve on their own

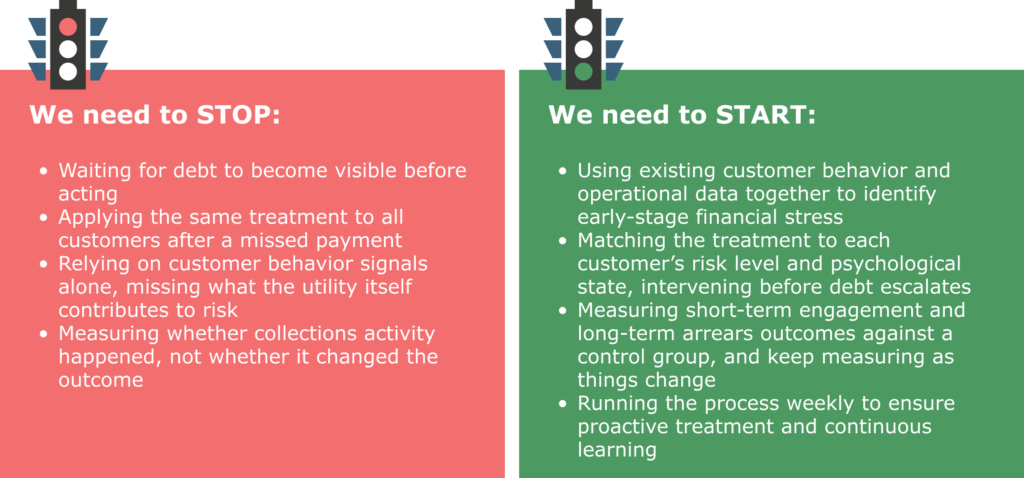

Traditional collections processes are built to respond only after the problem is visible. A customer misses a payment. A reminder is issued. Time passes. The balance grows. The customer moves through a defined pathway of notices, escalation, support options, and, ultimately, more serious collection activity.

There is nothing inherently wrong with that process. Utilities need fair, consistent, and compliant ways to manage overdue accounts. But the process is not designed to answer a different question: which customers are quietly moving toward long-term arrears before the balance tells the full story?

That is where predictive AI changes the model.

Mike Crooks, co-founder of SmartMeasures, opened this section of our recent Chartwell webinar with two points he wanted utilities to hear clearly.

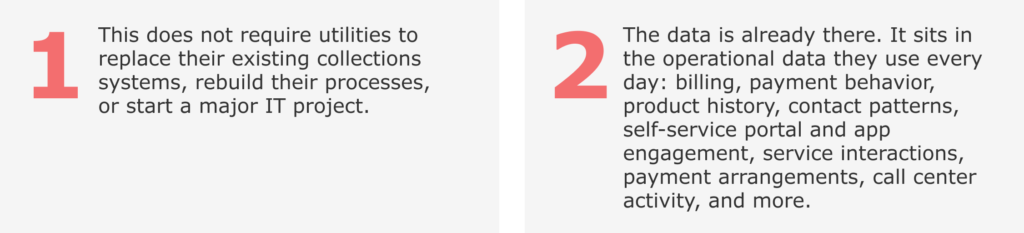

The opportunity is not to collect more data. It is to read the right patterns in the large collection of data that already exists. Typically, 3,000 to 4,000 signals per customer. At scale, patterns that are invisible to any individual collections officer become detectable.

Financial stress leaves behavioral fingerprints.

Some of those fingerprints are obvious: missed or delayed payments, broken arrangements, or a growing overdue balance. But the more useful signals are more subtle and often appear earlier, before standard collections triggers would classify a customer as high risk.

Examples of these more subtle signals are: a change in payment behavior, a shift in self-service use, a different pattern of contact behavior, and the billing cycle. Even the day of the month a bill is issued has predictive power.

And then there is a category of signals that Mike’s framing in the webinar made explicit: the signals based on the utilities practices and processes: price rise notifications, timing of a bill, the product a customer is on, the acquisition channel, outbound communications. As Mike puts it, these are signals based on what the utility “inflicts on the customer”.

Considering both behavioral and operational signals together can reveal customers whose risk is starting to change well before the account shows it. That is an important shift. A customer’s risk is not shaped only by their personal circumstances.

“It’s not just the financial signals. You need to look at both what the customer does and what the utility inflicts on the customer.” Mike Crooks, Co-Founder, SmartMeasures

Prediction is only the first step

Knowing who is at risk does not, change the outcome by itself. This is where many analytics projects fall short. A model may generate a useful list of customers, a score, or an insight. But unless that insight is converted into the right action, at the right time, in the right way, the collections result will not materially change.

As Article 3 in this series explored, customers in financial difficulty are not one homogeneous group and the psychological difference between them shapes what works. The Unexpected are new to hardship, feeling high shame, avoiding contact. The Stretched are familiar with debt, resigned, needing practical support without over-empathy. The Reluctant are strategically disengaged, requiring a different lever entirely. Sending the same message to all three is efficient. It is not effective.

The first AI identifies which customers are most likely to be in early stages of financial stress and determines their customer debt type. Next, treatment strategies must be designed by behavioral scientists, calibrated to the specific debt type and psychological state of each customer. A second AI then allocates the best treatment to each at-risk customer that is most likely to deliver the best outcomes for the customer and the utility. Prediction and allocation are different problems. They benefit from different AI techniques.

Standard governance and compliance frameworks still apply. Messages should still be sent through existing delivery platforms to ensure compliance and maintain the records and auditability the organization needs. Support programs still need to operate. Collections processes still need to run. Predictive intervention does not switch those systems off. It makes them work with greater precision.

The weekly rhythm and why it matters

Customer circumstances change. Data changes. Behavior changes. The business environment changes. An approach that runs as an occasional campaign will quickly lose relevance.

The system needs to operate as an automated weekly cycle: refresh the data, identify at-risk customers, allocate the right treatment, measure the outcomes, and the whole system should keep learning and adapting.

As Mike noted in the webinar, messages that work today may not work in six months. The weekly rhythm is what keeps the system current and what allows it to keep improving.

Measuring what matters

Testing against control groups is not optional. It is the only reliable way to know whether the intervention is working, and, critically, to detect when effectiveness declines. Without control groups, it is too easy to confuse activity with effectiveness. Control groups allow you to demonstrate the impact and business benefits achieved, regardless of other initiatives underway.

The right measures include both short-term and long-term indicators.

Short-term indicators: tell you whether the intervention is creating movement: uplift in inbound contact, increased self-service use, customers entering support programs, or changed payment behavior even without direct contact. These are the lead indicators that tell you whether the program is on track.

Long-term indicators: tell you whether the business outcome has changed and we are delivering a business benefit: fewer accounts moving into collections, lower cost-to-collect, reductions in long-term debt and write-offs.

The collections system does not need to work harder.

It needs to understand the customers better and act sooner.

The final article in this series looks at what leading utilities are already doing differently, and what the shift from collections to prevention looks like in practice.

Rebecca Wilson MSc (Business Psychology) is a Business Psychologist and Behavioural Science specialist at SmartMeasures.

SmartMeasures helps energy retailers and utilities reduce customer debt and improve retention through predictive AI and behavioral science.

For utilities exploring how to identify early-stage financial stress sooner, a low-risk Proof of Value pilot can test the approach using your existing data, systems, and governance frameworks, with results measured against a control group.

To continue the conversation from the webinar, contact us at [email protected].